g)@

Notes to the Consolidated Financial Statements

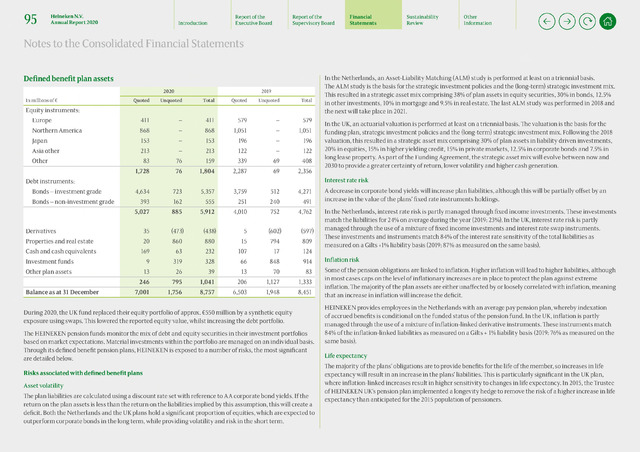

Defined benefit plan assets

Japan

Other

Q H Heineken N.V. Report of the Report of the Financial Sustainability Other

s \J Annual Report 2020 Introduction Executive Board Supervisory Board Statements Review Information

In millions of

2020

2019

Quoted

Unquoted

Total

Quoted

Unquoted

Total

Equity instruments:

Europe

411

411

579

579

Northern America

868

868

1,051

1,051

153

153

196

196

Asia other

213

213

122

122

83

76

159

339

69

408

1,728

76

1,804

2,287

69

2,356

Debt instruments:

Bonds - investment grade

4,634

723

5,357

3,759

512

4,271

Bonds - non-investment grade

393

162

555

251

240

491

5,027

885

5,912

4,010

752

4,762

Derivatives

35

(473)

(438)

5

(602)

(597)

Properties and real estate

20

860

880

15

794

809

Cash and cash equivalents

169

63

232

107

17

124

Investment funds

9

319

328

66

848

914

Other plan assets

13

26

39

13

70

83

246

795

1,041

206

1,127

1,333

Balance as at 31 December

7,001

1,756

8,757

6,503

1,948

8,451

During 2020, the UK fund replaced their equity portfolio of approx. €550 million by a synthetic equity

exposure using swaps. This lowered the reported equity value, whilst increasing the debt portfolio.

The HEINEKEN pension funds monitor the mix of debt and equity securities in their investment portfolios

based on market expectations. Material investments within the portfolio are managed on an individual basis.

Through its defined benefit pension plans, HEINEKEN is exposed to a number of risks, the most significant

are detailed below.

Risks associated with defined benefit plans

Asset volatility

The plan liabilities are calculated using a discount rate set with reference to AA corporate bond yields. If the

return on the plan assets is less than the return on the liabilities implied by this assumption, this will create a

deficit. Both the Netherlands and the UK plans hold a significant proportion of equities, which are expected to

outperform corporate bonds in the long term, while providing volatility and risk in the short term.

In the Netherlands, an Asset-Liability Matching (ALM) study is performed at least on a triennial basis.

The ALM study is the basis for the strategic investment policies and the (long-term) strategic investment mix.

This resulted in a strategic asset mix comprising 38% of plan assets in equity securities, 30% in bonds, 12.5%

in other investments, 10% in mortgage and 9.5% in real estate. The last ALM study was performed in 2018 and

the next will take place in 2021.

In the UK, an actuarial valuation is performed at least on a triennial basis. The valuation is the basis for the

funding plan, strategic investment policies and the (long-term) strategic investment mix. Following the 2018

valuation, this resulted in a strategic asset mix comprising 30% of plan assets in liability driven investments,

20% in equities, 15% in higher yielding credit, 15% in private markets, 12.5% in corporate bonds and 7.5% in

long lease property. As part of the Funding Agreement, the strategic asset mix will evolve between now and

2030 to provide a greater certainty of return, lower volatility and higher cash generation.

Interest rate risk

A decrease in corporate bond yields will increase plan liabilities, although this will be partially offset by an

increase in the value of the plans' fixed rate instruments holdings.

In the Netherlands, interest rate risk is partly managed through fixed income investments. These investments

match the liabilities for 24% on average during the year (2019: 23%). In the UK, interest rate risk is partly

managed through the use of a mixture of fixed income investments and interest rate swap instruments.

These investments and instruments match 84% of the interest rate sensitivity of the total liabilities as

measured on a Gilts +1% liability basis (2019: 87% as measured on the same basis).

Inflation risk

Some of the pension obligations are linked to inflation. Higher inflation will lead to higher liabilities, although

in most cases caps on the level of inflationary increases are in place to protect the plan against extreme

inflation. The majority of the plan assets are either unaffected by or loosely correlated with inflation, meaning

that an increase in inflation will increase the deficit.

HEINEKEN provides employees in the Netherlands with an average pay pension plan, whereby indexation

of accrued benefits is conditional on the funded status of the pension fund. In the UK, inflation is partly

managed through the use of a mixture of inflation-linked derivative instruments. These instruments match

84% of the inflation-linked liabilities as measured on a Gilts 1% liability basis (2019: 76% as measured on the

same basis).

Life expectancy

The majority of the plans' obligations are to provide benefits for the life of the member, so increases in life

expectancy will result in an increase in the plans' liabilities. This is particularly significant in the UK plan,

where inflation-linked increases result in higher sensitivity to changes in life expectancy. In 2015, the Trustee

of HEINEKEN UK's pension plan implemented a longevity hedge to remove the risk of a higher increase in life

expectancy than anticipated for the 2015 population of pensioners.

{kind=link}