106

Notes to the Consolidated Financial Statements (continued)

26. Employee benefits (continued)

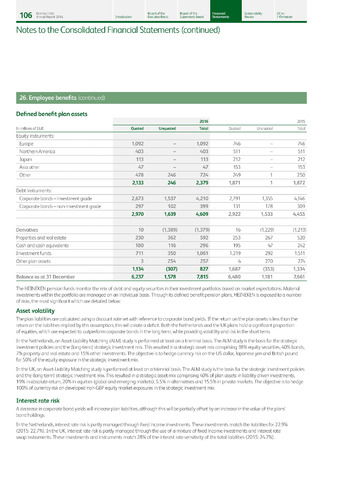

Defined benefit plan assets

-

-

-

-

-

-

-

-

Asset volatility

Interest rate risk

Heineken NV.

Report of the

Report of the

Financial

Sustainability

Other

Annual Report 2016

Introduction

Executive Board

Supervisory Board

Statements

Review

Information

2016

2015

In millions of EUR

Quoted

Unquoted

Total

Quoted

Unquoted

Total

Equity instruments:

Europe

1,092

1,092

746

746

Northern America

403

403

511

511

Japan

113

113

212

212

Asia other

47

47

153

153

Other

478

246

724

249

1

250

2,133

246

2,379

1,871

1

1,872

Debt instruments:

Corporate bonds - investment grade

2,673

1,537

4,210

2,791

1,355

4,146

Corporate bonds - non-investment grade

297

102

399

131

178

309

2,970

1,639

4,609

2,922

1,533

4,455

Derivatives

10

(1,389)

(1,379)

16

(1,229)

(1,213)

Properties and real estate

230

362

592

253

267

520

Cash and cash equivalents

180

116

296

195

47

242

Investment funds

711

350

1,061

1,219

292

1,511

Other plan assets

3

254

257

4

270

274

1,134

(307)

827

1,687

(353)

1,334

Balance as at 31 December

6,237

1,578

7,815

6,480

1,181

7,661

The HEINEKEN pension funds monitor the mix of debt and equity securities in their investment portfolios based on market expectations. Material

investments within the portfolio are managed on an individual basis. Through its defined benefit pension plans, HEINEKEN is exposed to a number

of risks, the most significant which are detailed below:

The plan liabilities are calculated using a discount rate set with reference to corporate bond yields. If the return on the plan assets is less than the

return on the liabilities implied by this assumption, this will create a deficit. Both the Netherlands and the UK plans hold a significant proportion

of equities, which are expected to outperform corporate bonds in the long term, while providing volatility and risk in the short term.

In the Netherlands, an Asset-Liability Matching (ALM) study is performed at least on a triennial basis. The ALM study is the basis for the strategic

investment policies and the (long-term) strategic investment mix. This resulted in a strategic asset mix comprising 38% equity securities, 40% bonds,

7% property and real estate and 15% other investments. The objective is to hedge currency risk on the US dollar, Japanese yen and British pound

for 50% of the equity exposure in the strategic investment mix.

In the UK, an Asset-Liability Matching study is performed at least on a triennial basis. The ALM study is the basis for the strategic investment policies

and the (long-term) strategic investment mix. This resulted in a strategic asset mix comprising 40% of plan assets in liability driven investments,

19% in absolute return, 20% in equities (global and emerging markets), 5.5% in alternatives and 15.5% in private markets. The objective is to hedge

100% of currency risk on developed non-GBP equity market exposures in the strategic investment mix.

A decrease in corporate bond yields will increase plan liabilities, although this will be partially offset by an increase in the value of the plans'

bond holdings.

In the Netherlands, interest rate risk is partly managed through fixed income investments. These investments match the liabilities for 22.9%

(2015: 22.7%). In the UK, interest rate risk is partly managed through the use of a mixture of fixed income investments and interest rate

swap instruments. These investments and instruments match 28% of the interest rate sensitivity of the total liabilities (2015: 24.7%).

{kind=link}