Financial Review

35

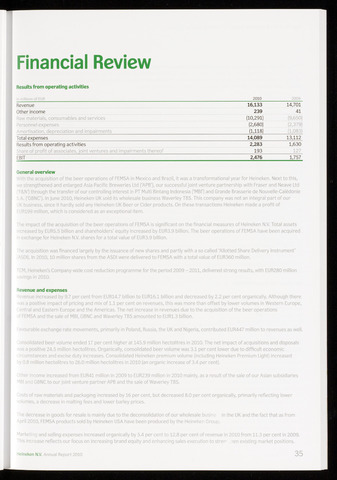

Results from operating activities

2010

Revenue

16,133

14,701

Other income

239

41

Raw materials, consumables and services

(10,291)

(9,650)

Personnel expenses

(2,680)

(2,379)

Amortisation, depreciation and impairments

(1,118)

(1,083)

Total expenses

14,089

13,112

Results from operating activities

2,283

1,630

Share of profit of associates, joint ventures and impairments thereof

193

127

EBIT

2,476

1,757

Seneral overview

With the acquisition of the beer operations of FEMSA in Mexico and Brazil, it was a transformational year for Heineken. Next to this,

we strengthened and enlarged Asia Pacific Breweries Ltd ('APB'), our successful joint venture partnership with Fraser and Neave Ltd

('F&N') through the transfer of our controlling interest in PT Multi Bintang Indonesia ('MBI') and Grande Brasserie de Nouvelle-Calédonie

S.A. ('GBNC'). In June 2010, Heineken UK sold its wholesale business Waverley TBS. This company was not an integral part of our

UK business, since it hardly sold any Heineken UK Beer or Cider products. On these transactions Heineken made a profit of

EUR199 million, which is considered as an exceptional item.

The impact of the acquisition of the beer operations of FEMSA is significant on the financial measures of Heineken N.V. Total assets

increased by EUR5.5 billion and shareholders' equity increased by EUR3.9 billion. The beer operations of FEMSA have been acquired

in exchange for Heineken N.V. shares for a total value of EUR3.9 billion.

The acquisition was financed largely by the issuance of new shares and partly with a so called 'Allotted Share Delivery Instrument'

(ASDI). In 2010,10 million shares from the ASDI were delivered to FEMSA with a total value of EUR360 million.

TCM, Heineken's Company-wide cost reduction programme for the period 2009 - 2011, delivered strong results, with EUR280 million

savings in 2010.

evenue and expenses

Revenue increased by 9.7 per cent from EUR14.7 billion to EUR16.1 billion and decreased by 2.2 per cent organically. Although there

was a positive impact of pricing and mix of 1.1 per cent on revenues, this was more than offset by lower volumes in Western Europe,

Central and Eastern Europe and the Americas. The net increase in revenues due to the acquisition of the beer operations

of FEMSA and the sale of MBI, GBNC and Waverley TBS amounted to EUR1.3 billion.

Favourable exchange rate movements, primarily in Poland, Russia, the UK and Nigeria, contributed EUR447 million to revenues as well.

Consolidated beer volume ended 17 per cent higher at 145.9 million hectolitres in 2010. The net impact of acquisitions and disposals

was a positive 24.5 million hectolitres. Organically, consolidated beer volume was 3.1 per cent lower due to difficult economic

circumstances and excise duty increases. Consolidated Heineken premium volume (including Heineken Premium Light) increased

by 0.8 million hectolitres to 26.0 million hectolitres in 2010 (an organic increase of 3.4 per cent).

Other income increased from EUR41 million in 2009 to EUR239 million in 2010 mainly, as a result of the sale of our Asian subsidiaries

MBI and GBNC to our joint venture partner APB and the sale of Waverley TBS.

Costs of raw materials and packaging increased by 16 per cent, but decreased 8.0 per cent organically, primarily reflecting lower

volumes, a decrease in malting fees and lower barley prices.

The decrease in goods for resale is mainly due to the deconsolidation of our wholesale busine in the UK and the fact that as from

April 2010, FEMSA products sold by Heineken USA have been produced by the Heineken Group.

Marketing and selling expenses increased organically by 5.4 per cent to 12.8 per cent of revenue in 2010 from 11.3 per cent in 2009.

rhis increase reflects our focus on increasing brand equity and enhancing sales execution to strep- men existing market positions.

Heineken N.V. Annual Report 2010

{kind=link}