15. Intangible assets

Brands and customer-related/contract-based intangibles

Capitalised borrowing costs

Financial Statements

Notes to the consolidated financial statements

The main brands capitalised are the brands acquired in 2008: Fosters, Strongbow and Sagres. The main

customer-related and contract-based intangibles were acquired in 2008 and are related to customer

relationships with pubs or retailers in the UK, Finland and Portugal (constituting either by way of a contractual

agreement or by way of non-contractual relations) and the licence agreement with FEMSA Cerveza (extended

in 2008 for 10 years).

Of the total amortisation charge of EUR61 million (2008: EUR42 million) for customer-related and contract-

based intangibles EUR43 million (2008: EUR33 million) is related to customer-related intangibles and

EUR 18 million (2008: EUR 9 million) to contract-based intangibles.

During 2009 no borrowing costs were capitalised (refer to the change in accounting policies, note 3b).

Impairment tests for cash-generating units containing goodwill

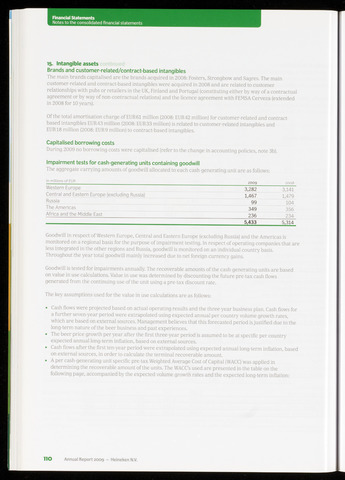

The aggregate carrying amounts of goodwill allocated to each cash-generating unit are as follows:

In millions of EUR 2009 2008

Western Europe

3,282

3,141

Central and Eastern Europe (excluding Russia)

1,467

1,479

Russia

99

104

The Americas

349

356

Africa and the Middle East

236

234

5,433

5,314

Goodwill in respect of Western Europe, Central and Eastern Europe (excluding Russia) and the Americas is

monitored on a regional basis for the purpose of impairment testing. In respect of operating companies that are

less integrated in the other regions and Russia, goodwill is monitored on an individual country basis.

Throughout the year total goodwill mainly increased due to net foreign currency gains.

Goodwill is tested for impairments annually. The recoverable amounts of the cash-generating units are based

on value in use calculations. Value in use was determined by discounting the future pre-tax cash flows

generated from the continuing use of the unit using a pre-tax discount rate.

The key assumptions used for the value in use calculations are as follows:

Cash flows were projected based on actual operating results and the three-year business plan. Cash flows for

a further seven-year period were extrapolated using expected annual per country volume growth rates,

which are based on external sources. Management believes that this forecasted period is justified due to the

long-term nature of the beer business and past experiences.

The beer price growth per year after the first three-year period is assumed to be at specific per country

expected annual long-term inflation, based on external sources.

Cash flows after the first ten-year period were extrapolated using expected annual long-term inflation, based

on external sources, in order to calculate the terminal recoverable amount.

A per cash-generating unit specific pre-tax Weighted Average Cost of Capital (WACC) was applied in

determining the recoverable amount of the units. The WACC's used are presented in the table on the

following page, accompanied by the expected volume growth rates and the expected long-term inflation:

IIO Annual Report 2009 - Heineken N.V.

{kind=link}