I Financial Statements 01

Notes to the consolidated financial statements

3 Significant accounting policies

differences arising on the retranslation of available-for-sale (equity) investments. Non-monetary assets

and liabilities denominated in foreign currencies that are measured at cost remain translated into the

functional currency at historical exchange rates.

(ii) Foreign operations

The assets and liabilities of foreign operations, including goodwill and fair value adjustments arising

on consolidation, are translated to Euro at exchange rates at the balance sheet date. The revenue and

expenses of foreign operations are translated to Euro at exchange rates approximating the exchange

rates ruling at the dates of the transactions.

Foreign currency differences are recognised directly in equity as a separate component. Since 1

January 2004, the date of transition to IFRS, such differences have been recognised in the translation

reserve. The cumulative currency differences at the date of transition to IFRS were deemed to be

zero. When a foreign operation is disposed of, in part or in full, the relevant amount in the translation

reserve is transferred to the income statement.

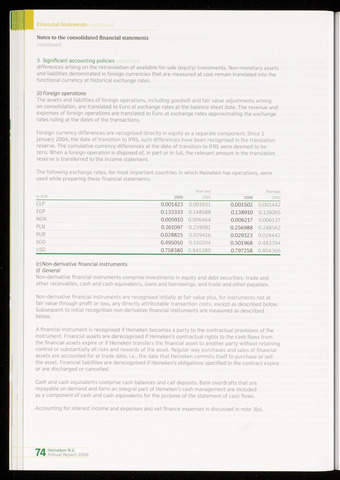

The following exchange rates, for most important countries in which Fleineken has operations, were

used while preparing these financial statements:

Year end Average

In EUR2006200520062005

CLP 0.001423 0.001651 0.001502 0.001442

EGP 0.133333 0.148588 0.138910 0.139265

NGN 0.005910 0.006464 0.006217 0.006137

PLN 0.261097 0.259081 0.256988 0.248562

RUB 0.028825 0.029416 0.029323 0.028442

SGD 0.495050 0.510204 0.501968 0.483394

USD 0.758380 0.845380 0.797258 0.804366

(c) Non-derivative financial instruments

(i) General

Non-derivative financial instruments comprise investments in equity and debt securities, trade and

other receivables, cash and cash equivalents, loans and borrowings, and trade and other payables.

Non-derivative financial instruments are recognised initially at fair value plus, for instruments not at

fair value through profit or loss, any directly attributable transaction costs, except as described below.

Subsequent to initial recognition non-derivative financial instruments are measured as described

below.

A financial instrument is recognised if Heineken becomes a party to the contractual provisions of the

instrument. Financial assets are derecognised if Heineken's contractual rights to the cash flows from

the financial assets expire or if Fleineken transfers the financial asset to another party without retaining

control or substantially all risks and rewards of the asset. Regular way purchases and sales of financial

assets are accounted for at trade date, i.e., the date that Fleineken commits itself to purchase or sell

the asset. Financial liabilities are derecognised if Fleineken's obligations specified in the contract expire

or are discharged or cancelled.

Cash and cash equivalents comprise cash balances and call deposits. Bank overdrafts that are

repayable on demand and form an integral part of Fleineken's cash management are included

as a component of cash and cash equivalents for the purpose of the statement of cash flows.

Accounting for interest income and expenses and net finance expenses is discussed in note 3(o).

"7/1 Heineken N.V.

I *r Annual Report 2006

{kind=link}