Notes to the Balance Sheet and the Profit and Loss Account for the financial year 1986

48

The amounts stated in the notes are in thousands of guilders,

unless indicated otherwise.

The aggregate amounts referred to in Article 383, paragraph

1, Title 8, Book 2 of the Netherlands Civil Code, in respect

of the remuneration, etc. of members and former members

of the Executive Board and that of members and former

members of the Supervisory Council were 5,158 (1985:

5,125) and 327 (1985: 301) respectively.

Accounting policies for the valuation and the determination of

income

Shares in Group companies are valued at net asset value

according to the accounting policies followed as stated on

pages 33 and 34.

Accounts receivable from Group companies are stated at

par value.

Also stated at par value are:

Accounts receivable, Cash at bank and in hand, Long-term

debts and Current liabilities.

Negative differences between the price paid and the value

according to the stated policies upon the acquisition of Group

companies are debited to the General reserve. Positive

differences are credited to the Revaluation reserve.

The difference between the value of a Group company at

the beginning of the financial year and at the end of the

financial year is offset against the Revaluation reserve, in

so far as this does not relate to the changes in the paid-up

share capital, the earnings of and the dividends from this

Group company.

The Profit and Loss Account has been drawn up in

accordance with the accounting policies as stated on page 35.

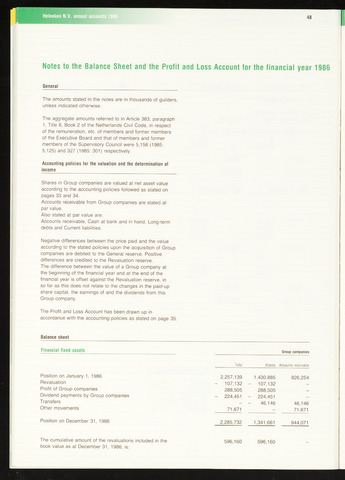

Balance sheet

Financial fixed assets Group companies

General

Total

Shares Amounts receivable

Position on January 1, 1986

Revaluation

Profit of Group companies

Dividend payments by Group companies

T ransfers

Other movements

2,257,139 1,430,885

107,132 - 107,132

288,505 288,505

224,451 - 224,451

- - 46,146

71,671

826,254

46,146

71,671

Position on December 311986

2,285,732 1,341,661

944,071

The cumulative amount of the revaluations included in the

book value as at December 31, 1986, is:

596,160

596,160

{kind=link}